RISK MANAGEMENT

(May 2022)

If the future could be predicted with 100% accuracy,

individuals and organizations could plan to completely avoid or flawlessly address

their exposures to loss. In reality, unknown events can upset even the best

predictions of performance and prevent individuals and organizations from

accomplishing tasks, meeting goals, or attaining expected results. The threat

of loss requires consideration of ways to deal with it and the consequences of

loss if it occurs.

Risk management is the method and discipline used to

address this uncertainty. In the last half of the twentieth century, risk

management developed from a group of vague, unorganized concepts, relying

heavily on common sense, to a highly developed and organized discipline that

enables organizations to anticipate losses and suggest actions to take to

prevent or reduce those losses.

What Is “Risk”?

Risk is the uncertainty,

possibility, or chance of loss. A chance occurrence that results in monetary

losses makes the profit predictions of an organization unreliable. Taken a step

further, such chance occurrences may expose the organization to a loss or

series of losses of a magnitude that could compromise its financial stability

and ability to survive.

Risk Management Defined

Risk management is the

active identification, evaluation and management of all potential hazards and

exposures to loss that a risk may experience. It incorporates insurance in the

process but also provides organized alternatives if insurance is not available,

inappropriate, or too expensive.

Risk management is a

continuous process of identifying loss exposures, measuring them against the

firm’s ability to tolerate them and then handling them with the appropriate

control, transfer, or financing techniques. Constant monitoring of exposures

and attention to them affects risk management decisions. Exposures identified

but not already addressed by a strategy must be reevaluated and decisions made

about the best methods for handling them.

In a current, broader concept

of Enterprise Risk Management, the goal includes using concepts that will allow

a business to identify and assess additional business opportunities with the

evaluation including how well that opportunity fits with the entity’s risk

appetite.

Types of Risk

Risk is either

speculative or pure. Speculative risk has two possible outcomes: the chance of

gain or the chance of loss. When a business commences operations, it will

experience only two possible outcomes over a period of time. It may be

successful and make money or it may lose money because income does not cover

expenses. Organizations deal with this type of risk by choice, actually seeking

or exposing themselves to certain risks with the hope of taking advantage of

opportunities. Speculative risk includes consideration of opportunity costs and

what might be lost by not taking a chance on a potentially profitable venture.

Risk managers involved with this type of risk must be able to evaluate

business, credit and commodity risks, hedging exposures and investment risks.

The other type, pure

risk, also offers two possible outcomes: loss or no loss. Examples of this type

of risk include loss to property by fire, wind, or theft; third party liability

claims for damages; or the interruption or reduction of income from loss of

power, strikes or fire. With pure risk, the most favorable outcome is to have

no loss. The only other possibility is that a loss will occur. This is why

exposures need to be identified and analyzed to determine the effect they may have

on continuing business operations. Whether identification and analysis take

place, the only two outcomes with pure risk situations are loss or no loss.

Risk managers involved with this type of risk must be knowledgeable and

experienced with insurance, various risk transfer clauses in operating

contracts, loss control and safety and accident prevention.

Pure risk exposures

involve a number of broad and diverse classes of risk. They include:

·

Economic

·

Legal

·

Political

·

Social

·

Physical

·

Juridical

Any or all of these can

present significant exposures to any organization. Pure and speculative risks

do not exist independent of one another. Both types exist and interact with one

another in varying degrees in most organizations. The focus of this article is

confined to pure risk exposures.

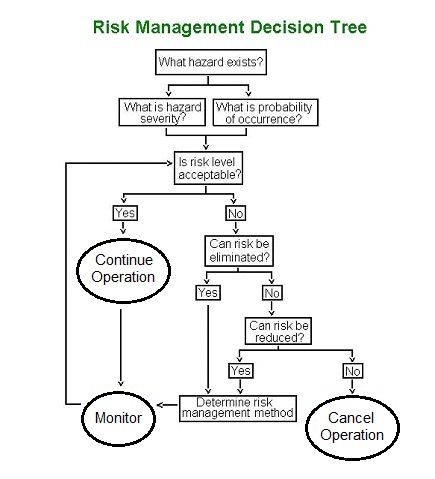

The Risk Management Process

The risk management

process consists of activities organized into five sequential steps or phases:

1. Risk

Identification

2. Risk

Analysis

3. Risk

Control

4. Risk

Financing and

5. Risk

Administration

1. Risk Identification

The first risk management

step is identifying the existing exposures to loss as well as exposures that

may exist in the future. This is accomplished by gathering information by any

number of methods, including survey forms, questionnaires, physical

inspections, product and procedure flow charts and contracts, financial records

and loss history reviews. These approaches attempt to discover the exposures to

loss faced by an organization. This phase is the foundation of risk management

since a risk not properly identified or addressed by the organization or an

individual is retained.

2. Risk Analysis

Once the exposures are

identified, they must be organized and quantified. This is accomplished in this

phase. Organizing risk, also known as the qualitative portion of the analysis

phase, requires reviewing and categorizing exposures into those sharing common

elements. One method is to place exposures into similar classes representing

potential losses, such as:

·

Property exposures

·

Liability exposures

·

Net income exposures

·

Human resource exposures

This phase also includes

quantifying the loss potential from the identified exposures. This is

accomplished by estimating the dollar amount of future losses that may occur.

One method of projecting future

losses is to review past loss experience, then use statistical probability and

trend analysis to extrapolate that past experience into estimated future

losses. Quantification also assists the risk manager in prioritizing the order

or sequence in handling possible loss exposures.

|

Example: The new Risk Manager for

Southwest Machine Manufacturers Unlimited has no idea about which loss

exposures need greater attention. She pores over the last ten years of the

company’s loss experiences and discovers the following: |

|

||

|

Situation A |

Situation B |

Situation C |

|

|

Property losses

occurred twice a year and each incident averaged $15,000 |

Fleet auto losses

occurred more than a dozen times a year and each incident averaged $6,000 |

Commercial General

Liability losses occurred about once every four years and averaged $45,000 |

|

|

Based on this

information, she decides to tackle the company’s auto losses. Although the

average loss per incident was far lower than the property and liability

losses, their annual frequency was much higher, resulting in the highest

amount of total annual loss. A total cost, $30,000. B total annual cost,

$48,000. C annual total cost, $11,250. |

|||

3. Risk Control

This is the action phase.

It includes any action taken, at the most optimal cost, to minimize or reduce losses

that may occur. The principal types of risk control methods most commonly used

in this phase are:

a. Avoidance

- Prevention

- Reduction

- Segregation

- Contractual

Transfer

Let's look at exactly

what is meant by each of these terms.

a. Avoidance

Avoidance is a decision to not engage in a particular

activity that creates an exposure to loss. It can also mean the elimination of

an activity that creates an exposure to loss.

|

|

Example: Jana, Acme Filters Inc.’s CFO, studies an offer to buy a

small filter company that has developed a new process meant to strengthen

filter fibers. Jana decides to decline the opportunity after research

discovers that the method would increase manufacturing costs by nearly 30%.

Further, the firm’s insurance records show that the process used has resulted

in worker injuries from chemical burns. Therefore, she avoids the exposure of

increased costs, a per unit, lower margin of profit and the higher worker

injury hazard. |

When a

risk is avoided, loss probability is zero. Be aware that this method is not

practical in all cases, since it could involve avoiding activities that might

be positive and result in profits. In the example above, Jana’s decision to not

invest in the stock also eliminates the chance to benefit from that stock’s possible

market gains.

Related

Article: The Cost of Doing Nothing

b. Prevention

Prevention

is any measure that reduces the probability or frequency of a particular loss

occurring but which does not completely eliminate all possibility of that loss

occurring. Prevention attempts to reduce the likelihood of an occurrence.

|

Example: The safety supervisor for Nifty Manufacturing adds

machine guards to their equipment in order to prevent access to moving parts

which could injure its machine operators. |

c. Reduction

Reduction

efforts attempt to reduce the severity of the losses that do occur. Wearing a

motorcycle helmet when riding does not stop the accident from happening, but it

should reduce injury to the rider if an accident does occur. This approach recognizes

that, since certain losses are inevitable and cannot be avoided or prevented,

they should be acknowledged and steps taken to minimize their impact.

d. Segregation

Segregation

consists of two techniques. The first is separation of loss exposure units and

it is used in conjunction with the second technique, which is the duplication

of loss exposure units. With separation, assets are divided into two or more

separate units. If they are then further separated geographically, the

likelihood of all assets being lost in a single event is greatly diminished.

Duplication, on the other hand, involves the reproduction of an asset to be a

standby kept in reserve. A common example of risk control by segregation is in

the use of computer backups. The backup disk becomes the duplication function

and storing the backup disk in a separate location is an example of the

separation function.

e. Contractual Transfer

Contractual

transfer is the shifting of a loss exposure in conjunction with an asset or

activity, using a written contract or agreement, from one party to another. In

contractual transfers for risk control, there is no indemnity or compensation

between the parties. The obligations for loss exposures resulting from the

performance of certain activities that one party deems hazardous are

transferred. An example of risk control by contractual transfer is the

outsourcing of a “risky” activity to an independent contractor.

|

Example: An automobile dealership service center accepts vehicles

requiring all types of repairs but arranges for independent contractors to

perform the painting and welding repairs. |

The risk control phase is

important but it only rarely eliminates risk unless avoidance is practiced. The

undesirable event may still occur and if it does, the organization will need

funds to pay for the damage caused by the loss. These funds are obtained

through the function of risk financing.

4. Risk Financing

Risk financing involves

acquiring funds at the lowest cost from which losses will be paid.

There are only two

answers to the question of who pays for damages caused by losses. In one case,

the organization experiencing the loss pays for the damages (risk retention).

In the other case, another person or a different organization pays for the

damages (risk transfer). There is a distinction between risk transfers made for

risk control and risk transfers made for risk financing. Risk control transfers

shift or transfer the acts or obligations to perform to another party. Risk

financing transfers shift the obligation to pay. It is possible to transfer the

obligation to perform a given act or process without transferring the

obligation to pay for losses as a result of the obligation to perform. The

reverse is also true and allows transfer of the obligation to pay without

transfer of the obligation to act. It is normal to transfer both the obligation

to act and the responsibility to pay losses arising from the transferred

obligation but it is not necessarily done that way in every case.

|

|

Example: A general contractor hires a sub-contractor to install

the heating and cooling equipment at a work site and the general contractor

is listed as an additional insured on the sub-contractor’s insurance policy. |

Financial risk transfer

is accomplished in one of two ways. One is to transfer it to a professional

risk bearer (an insurance company) by purchasing an insurance policy. The other

is to transfer it to someone other than an insurance company. The financial

transfer of risk to an insurance company is well known and understood and was

briefly discussed in the first part of this article. The financial transfer of

risk to a non-insurance entity is not necessarily as well known but is still

fairly common. Hold harmless agreements, indemnification clauses and liquidated

damages clauses are examples of frequently used risk financing transfer

clauses. They are found in a number of different written operating contracts,

such as lease agreements, customer sales agreements and agreements with

independent contractors. Other examples of financial risk transfers include the

obligation of a tenant to pay for plate glass damage or for the

repair/replacement of mechanical equipment damage to the landlord’s building.

Persuading another entity

to pay for losses may be desirable but the cost of actually doing so may be

prohibitive or impractical. As mentioned above, any risk not transferred is

retained. In many cases, it may be more cost-effective to retain certain risks

and the resulting damages and pay them like operating expenses. Losses that

occur frequently and predictably but which have fairly low dollar amounts

attached to them can usually be budgeted and efficiently financed internally

through risk retention. Other methods of risk retention and financing include

pre-loss funded and unfunded reserve accumulations and post-loss borrowing of

funds.

Defining and coordinating

financial risk transfer methods with financial risk retention methods is one of

the most challenging tasks confronting the risk manager. The ability to

anticipate losses, making arrangements to prevent, reduce or control their

impact and adequately arranging for funds availability to pay for them is the

reason the position exists and is one of the measures of the worth of the risk

manager to the organization.

Risk control and risk

financing activities interact with each other. An effective risk management

program must use at least one risk control technique and one risk financing

technique for each identified exposure.

5. Risk Administration

Risk administration is the

implementation and monitoring of risk management policies and procedures. Risk

administration covers a broad range of activities frequently assigned to the

risk management department. Some examples are:

·

Corporate planning

·

Policy development

·

Safety programs

·

Contingency and catastrophe planning

·

Crisis management

Other regular or frequent

administration activities include claims administration, allocation of the

costs of risk, litigation management, insurance acquisition, loss monitoring

and incident (near-miss) investigations.

How Does the Risk Manager Help?

The risk manager's job is

to identify and analyze risks and to make recommendations to management

concerning how to control and finance them. To do this effectively and

efficiently, the risk manager must be aware of all the activities, assets,

locations, products and processes of the organization. Risk managers must also

have knowledge of business law, statistics, economics, safety and loss control,

business finance and insurance. Most of all, the risk manager must be

innovative in applying this knowledge in the performance of his duties. The

risk manager is responsible for anticipating losses, adequately preparing the

organization for them and minimizing the costs of doing so.

Related Court Case: Loss Prevention Representative

Did Not Have Duty To Make Specific Inspection

The Role of Insurance in Risk Management

Insurance

is a component of risk management, not a substitute for it. In exchange for the

payment of a known loss (the premium), insurance transfers the financial

consequences of covered loss exposures from the insured to the insurance

company. This transfer of loss exposures by purchasing insurance to cover them

is the most common and frequently used method of handling risk. However, some

exposures are simply too trivial to justify the purchase of insurance and

others are so monumental, uncertain or uninsurable that no insurance carrier

will accept them. In addition, worldwide exposures, certain unique types of

risks and exposures created by government-enacted legislation are normally

avoided by most insurance companies. To summarize, insurance is simply not

available for many of the risks and exposures that organizations face. If

insurance for a given risk or exposure is not available, that risk or exposure

becomes retained by the insured and must be financed with funds from within the

organization if it causes a loss.

Insurance availability is

not the only reason to seek alternatives to handling risk. Organizations

monitor use of corporate funds closely because of the ever-present need to

maximize profits. If organizations do not use the most effective and efficient

methods of financing identified risk or loss exposures, they jeopardize their

competitive position in their marketplace and possibly their future survival.

Conclusion

Insurance may be the first or last way to handle risk but

it is not necessarily the only way or the best way. Risk management is a

comprehensive approach to handling risk by identifying, analyzing, controlling

and financing risk, and finding and implementing the most efficient methods for

doing so. The risk management function plans pre-loss activities, prepares the

organization for losses, and executes post-loss activities. When risk

management activities are done effectively and efficiently, they offer a

thorough and efficient approach for addressing the expenses and effects of

losses that face an organization.